Knowledge is power. There is no statement truer for knowing your financial situation. Knowing your credit score allows you to plan accordingly. It also provides an extra layer of protection against fraud and identity theft. Before we jump the gun, let’s go back to the basics.

What is a credit score?

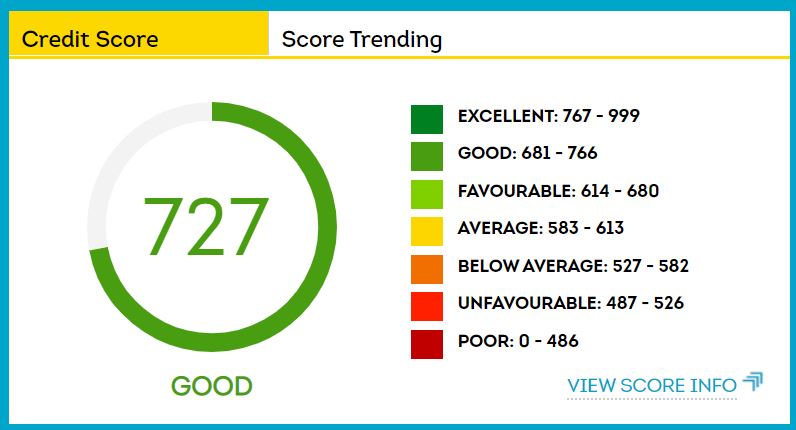

A credit score determines the creditworthiness of a consumer. Institutions use the score to evaluate consumers when applying for any credit like a loan, credit card, or clothing account. The scoring system is between poor to excellent, ranging from 0 – 999.

Credit Scoring System:

The higher you score, the more creditworthy the consumer appears to the credit provider. Meaning the consumers could qualify for credit or a loan.

What is a good credit score?

The type of credit you are applying for determines the credit score rating required. The institution you are applying at affects the rating required as well. Each institution has set requirements for different types of credit.

With that said, there is a score that is considered a good credit score. Any score above 680 is a good score. But applying for credit is not solely based on your credit rating. Other factors considered by institutions when applying for credit are income and expenses. Yet, it’s not limited to only those. To get a list of requirements, contact the institution you are considering.

Why should you check your credit score?

As mentioned before, knowing your credit score can protect you from fraud and identity theft. Here is how that works.

It keeps a record of your personal and financial information. Information like:

- Name and Surname

- ID number

- Dependants

- Employment

- Physical address

- Contact numbers

- Financial information like:

- Accounts

- Loans

- Credit

When you or any other financial institution, with your consent, checks your credit score, they have access to all that information. How does that help you protect against fraud and identity theft?

You, as the consumer, can view any notices, warnings, judgments, or defaults on your account that can affect your credit rating negatively. You can view who the institution is that placed the stain on it, allowing you to dispute the matter and get it corrected. That means you can view any fraudulent activity in your name. That includes the status of all your accounts and prevents scammers from using your identity.

How to get your credit score?

You get one free credit report yearly but, you pay for your credit rating. The difference between the two is that the one shows your credit rating and the other one doesn’t. Besides the score, there are no other differences. On both reports, you’ll find your notices, judgments, accounts information, and personal information. That gives you the opportunity to improve your credit rating without knowing your credit score. Here is a tutorial on how to get your free credit report.

Tips for improving your credit score?

Managing your credit score is easier than you think. But as the opening line of the article states, knowledge is power. Understanding your financial situation is the first step to managing your credit score. Knowing allows you to budget and plan accordingly.

Here are our top 3 tips to increase your credit rating.

- When considering applying for credit, don’t apply at multiple institutions. Each application will appear on your credit report for 24 months. That lowers your credit score rating for two years.

Fix – Do your research and choose the institution based on what they offer you. Look for lower interest rates, lengthier interest-free periods, and more benefits. Remember, you are spending your hard-earned money with that institution, and you don’t have to settle. - Never take too much credit. It’s tempting to take an R20 000 credit card when you earn R10 000 or R8 000 clothing account when you earn R15 000. What this does is tempt you into spending a big chunk of your income with that institution. Investing your money in your future can lead to improved earnings in the future.

Fix – Know the difference between what you want and what you need. What you can afford and what you are willing to spend. In my personal life, I never spend more than I can pay cash immediately on a clothing account. That means there are constant transactions on said account. Improving my credit score, and I don’t create any debt. - Financial institutions want you more indebted to their business. They offer you high value credit cards reducing your cash flow significantly. The consumer ends up paying interest for many years on the money they spent on a credit card years earlier. That lowers your credit score when the amount in your credit card is 35% less than the value of the credit card.

Example: Your credit card is to the value of R10 000, and the value in the credit card is less than R3 500 at the financial month-end.

Fix – Pay your credit card in full every month. I know this sounds crazy, but this works. It saves you money on interest and increases your credit score. Most credit cards have a 60-day interest-free period (read your T&C or contact the institution for your interest-free period). The interest-free period resets to the original length when you pay your credit card in full. Keep the money in that account for a short period before using your credit card.

If your credit card value is higher than your salary, it becomes harder to do this. So you will have to reduce your credit card systematically. That will affect your credit score less than keeping it lower than the 35% value.

Following these three tips will make a difference in your credit score and your financial life.

Bonus Credit Card tip:

Put more money than the limit of your credit card value in that account. You can use the credit card immediately, and it shows credit transactions. Plus, when you have credit card insurance, you are protected against card fraud when shopping. There is no fraud insurance available for cheque cards.

If you found this article helpful, share it with your family and friends. With financial knowledge, we can build a better South Africa. Leave a comment with your top financial tip or any questions you may have.

Leave a Reply